Reminder Medicare's Annual Enrollment Period runs October 15 – Dec

Medicare Annual Enrollment Period (AEP) Reminder

Every fall, millions of Medicare beneficiaries across the country have a limited window to review, change, or update their Medicare coverage. It's called the Annual Enrollment Period — and if you live in Clearwater, Largo, Palm Harbor, or anywhere in the Tampa Bay area, it's one of the most important dates on your calendar.

The problem is that most people let it pass without doing anything. They assume their current plan is fine, or they don't know where to start. That inaction can cost hundreds — sometimes thousands — of dollars over the course of the year.

This guide walks you through everything you need to know about the Medicare Annual Enrollment Period so you can make a confident, informed decision before the deadline.

What Is the Medicare Annual Enrollment Period?

The Medicare Annual Enrollment Period (AEP) — also called the Medicare Open Enrollment Period — runs every year from October 15 through December 7. Any changes you make during this window take effect on January 1 of the following year.

During AEP you can:

— Switch from Original Medicare to a Medicare Advantage plan — Switch from a Medicare Advantage plan back to Original Medicare — Change from one Medicare Advantage plan to another — Switch your Part D prescription drug plan — Add a Part D plan if you didn't have one before

This is the one time each year when most Medicare beneficiaries can make changes to their coverage without needing a qualifying life event.

Why You Should Review Your Plan Every Year — Even If You're Happy With It

This is the most important thing to understand: your plan changes every year, even if you don't.

Insurance carriers adjust their Medicare Advantage and Part D plans annually. That means your premiums, copays, deductibles, drug formulary, and provider network can all shift on January 1 — without you doing anything. A plan that was a perfect fit last year may not be the best option this year.

Here's what commonly changes:

— Premiums — your monthly cost may increase — Drug formulary — medications you take may move to a higher cost tier or be dropped from coverage entirely — Provider networks — your doctor or specialist may no longer be in-network — Extra benefits — dental, vision, or fitness benefits may change — Out-of-pocket maximum — your maximum annual exposure may increase

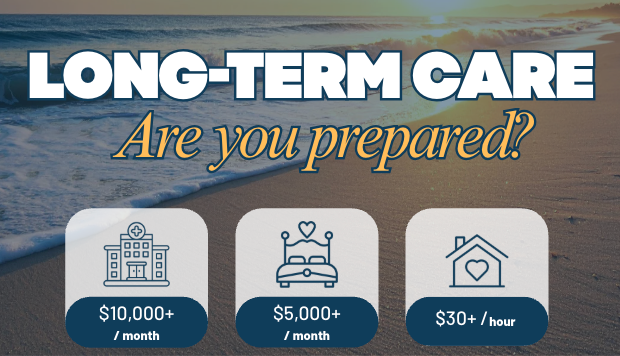

Taking 15–20 minutes to review your plan each fall can easily save you $500–$1,500 or more over the course of the year.

What to Look for When Reviewing Your Medicare Plan

When you sit down to review your coverage, here's what to focus on:

1. Your prescriptions Pull out a list of every medication you take, including dosage. Run them through the Medicare Plan Finder at medicare.gov to see how each plan covers your specific drugs and what your out-of-pocket cost would be.

2. Your doctors If you're on a Medicare Advantage plan, verify that your primary care doctor and any specialists you see are still in-network for the coming year. Networks change annually.

3. Your total cost — not just the premium A $0 premium plan may still cost you more than a plan with a modest premium if the copays and out-of-pocket maximum are higher. Look at the full picture.

4. Your benefits If your plan offered dental, vision, hearing, or over-the-counter benefits, confirm those benefits are continuing and at the same level.

5. Your Annual Notice of Change (ANOC) If you're currently on a Medicare Advantage or Part D plan, your carrier is required to mail you an Annual Notice of Change by September 30. This document outlines every change to your plan for the upcoming year. Read it carefully.

Common AEP Mistakes to Avoid

Doing nothing Staying in your current plan by default is a choice — and often not the best one. At minimum, read your ANOC and verify your drugs and doctors are still covered.

Only looking at the premium The monthly premium is one number. The out-of-pocket maximum, copays, and drug costs tell the rest of the story.

Missing the deadline AEP ends December 7 — no exceptions. If you miss it, you're locked into your plan until the next enrollment window (with limited exceptions for Special Enrollment Periods).

Not checking the drug formulary This is the most common and costly mistake. A medication that cost you $10/month under your old plan could cost $80–$150/month under a plan that places it on a higher tier.

Going it alone With dozens of plans available in Pinellas, Hillsborough, and Pasco County, comparing options on your own is overwhelming. A local independent broker can do the legwork for you — at no cost.

How TD Coverage Can Help During AEP

As an independent Medicare broker in Clearwater, FL, Trever Dahms is contracted with 70+ carriers and can compare every Medicare Advantage and Part D plan available in your area — side by side, with no pressure and no cost to you.

During AEP, Trever helps clients:

— Review their current plan against all available options — Check that their doctors and medications are covered — Identify plans with better benefits or lower total costs — Complete enrollment before the December 7 deadline

Whether you're brand new to Medicare or a long-time beneficiary who just wants a second opinion, the consultation is free and there's no obligation to switch.

Don't wait until December — the best plans fill up and schedules get busy.

📞 Call or text: (262) 352-3997

🌐 Visit: tdcoverage.com ]

📍 Serving Clearwater, Largo, Palm Harbor, Dunedin, St. Petersburg, Tampa, and all of Pinellas, Hillsborough, and Pasco County